In the fog of the video streaming wars, job losses and business closures are imminent

- Written by: John J Oliver, Professor of Strategic Media Management, Bournemouth University

Prussian general and military theorist Carl von Clausewitz[1] presented the concept of the “fog of war” in 1832. It is a phrase that has become synonymous with the uncertainty and confusion of military battle.

But this expression also acts as a useful metaphor to describe the industry and market dynamics that subscription video-on-demand streaming firms find themselves operating in – that is, uncertainty.

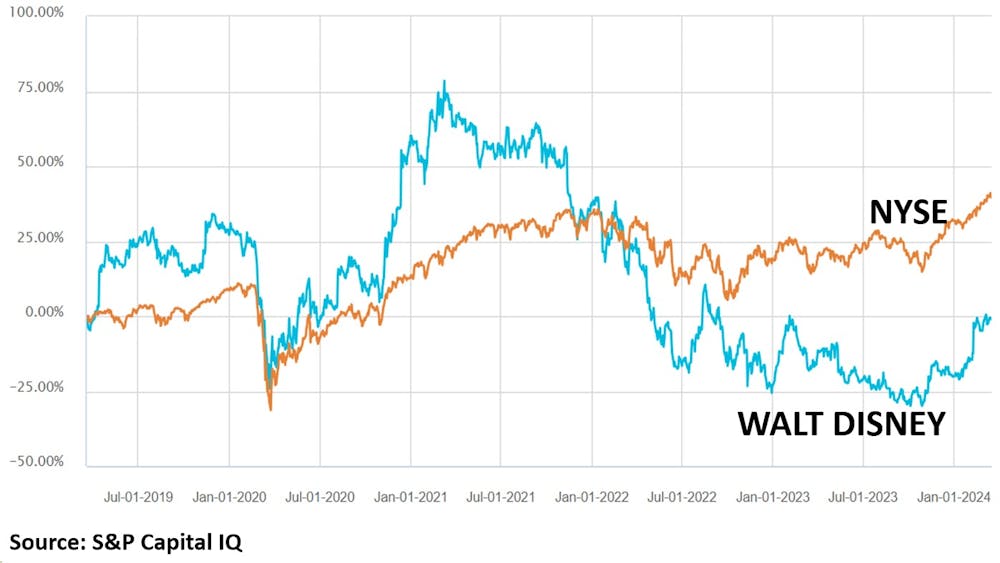

This uncertainty is demonstrated by the performance of American streaming platform Disney+. Since 2019, the platform has received US$10 billion[2] (£7.9 billion) of investment. But, over the same period, it has lost roughly 12 million customers[3], and it posted staggering losses of more than US$1.6 billion[4] in 2023.

In November, its parent company, Walt Disney, introduced[5] a new “cost-reduction strategy” that will aim to cut 7,000 jobs and save US$7.5 billion in the face of weakening economic conditions and tougher competition.

Five year share price comparison: Walt Disney v New York Stock Exchange

The COVID pandemic supercharged the on-demand streaming business as consumers sought to entertain themselves during the numerous lockdowns. The streaming industry experienced a period of rapid growth, attracting a flood of new entrants lured by market growth rates of 40% per year[7] and potentially high profits from surging consumer demand.

Companies such as Netflix, Amazon, Disney+ and Apple TV gained millions of customers in a matter of months and invested billions of dollars on new content, infrastructure and marketing. It all seemed too good to be true as the “land grab” for subscriber growth and market share continued into 2022.

However, an easing of lockdown restrictions saw consumers vacate their sofas and give up their binge-watching TV habits, ready to explore the great outdoors again.

The shakeout

The streaming industry is currently characterised by an oversupply of service providers. This has led to aggressive competitive pricing where businesses set their prices based on what their competitors are charging.

For example, instead of Netflix basing its subscription price solely on production costs and a desired profit margin, it will consider the prevailing prices offered by its rivals in the market and find a strategic price point that allows it to be competitive while also maintaining profitability.

Platforms with less efficient operations or inferior offerings are starting to struggle and an “industry shakeout” is inevitable. This is where a significant number of businesses are eliminated or acquired through competition in a period of intense consolidation.

Think of it as a metaphorical earthquake. The ground shifts beneath established players, forcing some to adapt, some to crumble, and others to emerge even stronger.

Take, for instance, the Swedish streaming platform, Viaplay. Despite being much smaller than its US counterparts, it adopted an expensive international expansion strategy[8] that was fuelled by the pandemic. This strategic approach failed and Viaplay could not expand profitably outside its home market.

The cost of living crisis then resulted in subscriber price increases and higher customer churn as a result. Uncertainty surrounding the firm has also been made worse by the sacking of its CEO and the introduction of a plan to significantly cut operating costs[9]. It’s no great surprise then that the company has withdrawn its long-term guidance for sales revenue and its share price has slumped[10] by a remarkable 99% over the past 12 months.

This shakeout phase of industry development will result in job losses and business closures until a situation develops where a smaller number of stronger, more efficient players dominate the industry through “scale advantage”.

A good example of consolidation occurred in the social media industry in the early 2000s. Platforms such as MySpace, Friendster and Friends Reunited gained early popularity with consumers, but then ceased trading or became a competitive insignificance as Facebook emerged as a dominant force. To maintain its market-leading position and access new users, Facebook went on to acquire smaller competitors including Instagram[11] and WhatsApp[12] in 2012 and 2014 respectively.

The benefits of this “scale advantage” are more efficient access to international markets, higher profitability and the ability to deliver lower subscription prices due to the economies of scale. This is particularly beneficial to consumers at a time of inflationary pressure on discretionary spend.

The outlook

So, who is at risk on the battlefield of streaming wars? Even household favourites such as Netflix, with a global market share of 24%, 260 million subscribers and best-in-class content are not safe.

Five year share price comparison: Netflix v Nasdaq

Netflix loses stream: investor confidence fizzles as growth slows.

S&P Capital IQ, CC BY-NC-SA[13]

Netflix loses stream: investor confidence fizzles as growth slows.

S&P Capital IQ, CC BY-NC-SA[13]

Given the current focus on corporate profitability in an industry likely to consolidate, Netflix’s ability to produce a net profit[14] of more than US$5 billion and an impressive operating margin of 21% in 2023 will make it a potential target for acquisition. This is particularly the case given that the size of the company, at US$264 billion, is relatively small compared to larger competitors such as Apple (US$2.75 trillion) and Amazon (US$1.84 trillion).

The “fog of streaming war” will clear and the strategic uncertainty caused by lower market growth rates, inflationary pressure and economic weakness will decrease. As such, competitive industry positions will become more established, normalised and defended.

The key question facing most media companies in the future will be how to make subscription video-on-demand streaming a profitable part of their business.

References

- ^ Carl von Clausewitz (www.britannica.com)

- ^ US$10 billion (www.ft.com)

- ^ 12 million customers (www.forbes.com)

- ^ US$1.6 billion (www.ft.com)

- ^ introduced (thewaltdisneycompany.com)

- ^ CC BY-NC-SA (creativecommons.org)

- ^ 40% per year (rm.coe.int)

- ^ strategy (www.ft.com)

- ^ cut operating costs (www.ft.com)

- ^ slumped (markets.ft.com)

- ^ Instagram (www.bbc.co.uk)

- ^ WhatsApp (www.bbc.co.uk)

- ^ CC BY-NC-SA (creativecommons.org)

- ^ net profit (s22.q4cdn.com)