how countries around the world are tackling the cost of living crisis

- Written by: Alan Shipman, Senior Lecturer in Economics, The Open University

The rising cost of living[1] is biting businesses and households around the world. Editors from across The Conversation’s international network have asked local academic experts to explain how their countries and regions are tackling this issue, as well as the 2023 outlook for prices and interest rates where they live.

This article is the third in our series on where the global economy is heading in 2023. It follows recent articles on inflation[2] and energy[3].

UK: recession on the horizon

At first sight, the UK’s cost of living crisis might look fairly mild compared to other countries. Its inflation rate was 10.7% in November 2022, compared to[4] 12.6% in Italy, 16.% in Poland and over 20% in Hungary and Estonia. But the Bank of England expects a recession in the UK this year – possibly lasting until mid-2024[5].

This is because the proportion of UK households that lack insulation against financial setbacks is unusually large for a wealthy economy. One pre-pandemic survey found that 3 million people in the UK would fall into poverty[6] if they missed one pay cheque, with the country’s high housing costs being a key source of vulnerability. Another recently suggested that one-third of UK adults would struggle[7] if their costs rose by just £20 a month.

The pandemic saw over 4 million households take on extra debt[8] with almost as many falling behind on repaying it. And recent jumps in energy and food bills will push many over the edge, especially if heating costs remain high when the present government cap on energy prices[9] ends in April.

UK governments have been stealthily raising taxes since 2010 and in real terms (adjusting for inflation) typical UK household income was already 2% lower in 2018 than in 2007[10]. But real incomes have been further eroded over the past year since the UK’s 10.7% inflation rate (as of November) is far above the pay increases many employees have had to settle for in recent months.

But recent events have forced the government to make decisions that were not necessarily aligned with the looming recession. In September 2022, Liz Truss became prime minister with bold pledges to cure the UK’s economic malaise[11]. The global financial markets responded dramatically to her tax cutting plans by hiking the interest they charge the UK government and businesses to borrow. This forced the newly installed chancellor Jeremy Hunt to embark on another round of public spending cuts and tax increases[12] in November – actions governments usually reserve for the height of a boom, not the eve of a slump.

Read more: How bonds work and why everyone is talking about them right now: a finance expert explains[13]

The Bank of England is also doing the opposite of what central banks prefer to do before a downturn. High inflation forced it to raise rates to 3.5% in December[15], with more rises expected in 2023. This boosts debt repayments for the millions who’ve borrowed to buy their homes, not to mention those with unsecured credit card or overdraft debt.

All of these additional costs subtract from a household’s disposable income. And because household consumption makes up close to 60%[16] of all spending in the UK economy, this will inevitably lead to recession – which could well turn out to be very painful and very long.

US: central bank signals caution

Inflation increased significantly[17] in the US in late 2021 and early 2022, reaching levels higher than at any time in the last 40 years. The Federal Reserve responded by aggressively raising its benchmark rate[18] (the federal funds rate) seven times since March in an effort to stabilise prices. A couple of smaller increases[19] are expected in 2023.

The US consumer price index, a standard measure of inflation, shows that prices peaked[20] in June 2022, increasing by 9.1% over the previous year. The index has decreased every month since June, with the November data – the most recent available – indicating that US prices are 7.1% over the prior 12 months.

The fed funds rate[21] serves as a benchmark for other interest rates, such as mortgage rates. Its recent increases have started to reduce demand for goods and services and investment. For example, existing home sales in November were 7.7% lower than in October[22] and are down over a third from a year earlier. The underlying reason is that mortgage interest rates have more than doubled to over 6%[23], after reaching 7% in October, from 3% in the beginning of 2021.

The ripple effects of the reduction in housing demand will continue to slow economic activity for months to come because some of the impacts of monetary policy occur with a lag.

The Fed is now signalling[25] that it will continue to raise interest rates in early 2023 before pausing, a cautious approach that is justified by a variety of economic data. This is partly due to continued strength in the labour market[26] as unemployment remains low, wages that haven’t been adjusted for inflation continuing to rise[27], and roughly 10 million jobs remaining open, according to the latest data. To the extent that companies have to raise wages to attract or keep workers, this may lead to higher prices and persistent inflation.

This issue is especially important given the ageing population[28] in the US and the effect it has on the labour market. At the same time, the recent fall in energy prices[29] is unlikely to continue, so further reductions in inflation will have to come from declines in other areas, such as shelter and food.

Australia and New Zealand: using restraint to ease inflation

The regular survey of economic forecasts published by The Conversation Australia at the start of 2022 was titled[30]: Top economists expect RBA to hold rates low in 2022 as real wages fall.

This forecast for how the Reserve Bank of Australia would set rates in 2022 was spectacularly wrong. The second part turned out to be pretty right: real wages did fall[31], although not because they continued to barely grow as the experts had been expecting, but because their growth was dwarfed by an explosion in inflation.

After hovering below the Reserve Bank’s 2-3% target band for most of the previous five years, Australia’s annual rate of inflation began 2022 at 3.5% but shot up to 5.1% in March after Russia invaded Ukraine and reached 7.3% for the year to September. The bank expects something close to 8%[32] for the year to December when the figures are next updated in late January.

Our World in Data, CC BY[44][45]

Energy issues aside, countries are also impacted by the global market[46] just like companies are affected by their institutional environment[47]. As a result, future changes in public policy could influence the inflation rate, which may or may not have peaked.

For example, the European Central Bank’s decision[48] to raise interest rates for the first time in a decade last July could weigh on countries’ budgets, giving governments less room for manoeuvre as they try to contain price increases.

Without some regional stability in terms of politics and economics, France may not be able to continue to outperform its neighbours in the coming months.

This is an edited excerpt from an article published in October 2022[49].

Spain: inflation, public spending, deficit and debt

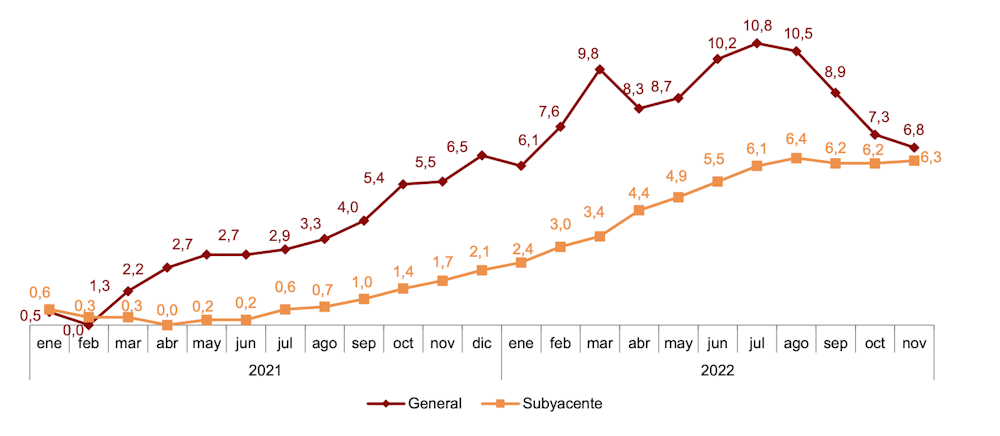

After beginning 2022 with inflation at 6.1%[50], Spain’s consumer price index peaked at 10.8% in July before closing out the year at a rate of 6.8%. Taking into account the 2021 inflation journey from 0.5% in January, to 2.9% in July and 6.5% in December, it now looks like price rises are being brought under control.

Core inflation (which excludes unprocessed food and energy) saw a more gradual but sustained rise. It was 2.4% in January 2022, peaked at 6.4% in August and fell to 6.3% in November. The closing gap with headline inflation during the final quarter of last year was mainly due to government measures to control the rise in energy prices[51].

Inflation in Spain, 2021-2022

Our World in Data, CC BY[44][45]

Energy issues aside, countries are also impacted by the global market[46] just like companies are affected by their institutional environment[47]. As a result, future changes in public policy could influence the inflation rate, which may or may not have peaked.

For example, the European Central Bank’s decision[48] to raise interest rates for the first time in a decade last July could weigh on countries’ budgets, giving governments less room for manoeuvre as they try to contain price increases.

Without some regional stability in terms of politics and economics, France may not be able to continue to outperform its neighbours in the coming months.

This is an edited excerpt from an article published in October 2022[49].

Spain: inflation, public spending, deficit and debt

After beginning 2022 with inflation at 6.1%[50], Spain’s consumer price index peaked at 10.8% in July before closing out the year at a rate of 6.8%. Taking into account the 2021 inflation journey from 0.5% in January, to 2.9% in July and 6.5% in December, it now looks like price rises are being brought under control.

Core inflation (which excludes unprocessed food and energy) saw a more gradual but sustained rise. It was 2.4% in January 2022, peaked at 6.4% in August and fell to 6.3% in November. The closing gap with headline inflation during the final quarter of last year was mainly due to government measures to control the rise in energy prices[51].

Inflation in Spain, 2021-2022

Spain’s Consumer Price Index (the figure for November 2022 refers to the leading indicator).

National Statistics Institute (INE), Spain[52]

Like many other countries, Spain lacks control and efficiency[53] when it comes to public spending. The country’s pension system[54] must support a rapidly growing older population; it is highly dependent on fossil fuels; the unemployment rate has been above 10%[55] since 2008; and – again like other countries – it is suffering from deep political and social polarisation right now. A high public deficit[56] has also helped inflate the Spanish debt bubble[57].

Spain’s Consumer Price Index (the figure for November 2022 refers to the leading indicator).

National Statistics Institute (INE), Spain[52]

Like many other countries, Spain lacks control and efficiency[53] when it comes to public spending. The country’s pension system[54] must support a rapidly growing older population; it is highly dependent on fossil fuels; the unemployment rate has been above 10%[55] since 2008; and – again like other countries – it is suffering from deep political and social polarisation right now. A high public deficit[56] has also helped inflate the Spanish debt bubble[57].