Interest rates are likely to rise by much less than most people are predicting

- Written by: Costas Milas, Professor of Finance, University of Liverpool

Inflation was already a serious problem thanks to the bottlenecks[1] in the global supply chain caused by the COVID-19 pandemic. But following Russia’s brutal invasion of Ukraine, and the effect on oil and gas prices, inflationary pressures now look a whole lot worse.

The big question is how central banks will respond. Raised inflation demands higher interest rates, but this risks compounding the global economic damage[2] likely to be caused by the western sanctions against Russia. The Bank of England has been slightly ahead of the curve on tightening monetary policy, having raised the policy rate of interest twice in the last couple of months to reach 0.5%[3] and also ending its quantitative easing (QE) programme[4] for increasing the money supply back in December.

The Fed’s QE programme is only coming to an end now, while it has yet to raise interest rates. So with both the Fed and Bank of England about to make their latest monthly decisions, what can we expect?

The story so far

UK consumer price inflation currently stands[5] at 5.5%, more than twice the Bank of England’s 2% inflation target, and it is expected[6] to peak at 7% in April or even higher[7] if there is a sustained surge in energy prices. US inflation, meanwhile, is already nudging 8%[8].

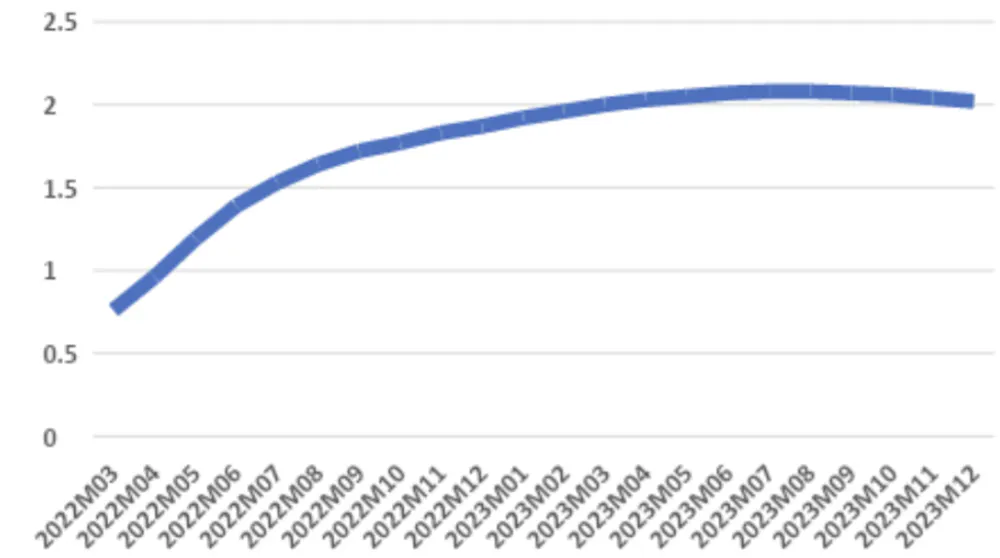

Financial markets currently expect[9] the Bank of England’s Monetary Policy Committee (MPC) to raise the policy rate of interest to 0.75% on March 17 en route to[10] a peak of 2% a year from now, where it is expected to remain until the end of 2023. The US equivalent rate is at 0.25%. It is likely to be increased at the latest meeting for the first time in this cycle by 0.25 or 0.5 points, before possibly heading towards 2%[11] by year end.

Market expectations of UK interest rate (%)

Author provided

My policy tool assumes that inflation remains as high as 3.1% in the first quarter of 2024 – significantly higher[23] than the 2.15% forecast made by the Bank of England prior to the Ukraine invasion. It also assumes that inflation reverts back to the 2% target by the end of 2024.

The tool also assumes a negative effect on UK economic growth: 1 percentage point less than its potential growth in the second and third quarters. This is from raised energy prices, the government’s decision to phase out[24] Russian oil imports by the end of 2022 and general elevated uncertainty related to the war. (It is worth noting that the UK gets around 4%[25] of its gas and around 11%[26] of its oil from Russia.)

As far as the aggregate risk index is concerned, the assumption is that the current crisis does not escalate to a widespread, persistent war. I’m assuming that the index rises to 0.35 in mid-2022 before reverting to zero by the end of 2023.

What happens next

Based on these assumptions, I expect that the MPC’s latest meeting will increase UK interest rates, in line with market expectations, to close to 0.75%. But it will then raise them to just 1.3% by the end of 2023 – considerably less than what financial markets predict. And though I don’t project US rates in the same way, it might be reasonable to expect decisions from the Fed to follow a similar trajectory.

As far as the UK is concerned, different assumptions of the policy tool obviously lead to different interest rate predictions. For example, some might argue that my 10% weighting for geopolitical risk in the total aggregate risk calculation is too low. After all, in 2001 the MPC responded to the 9/11 attacks by holding a special meeting[27] in which it cut the policy rate from 5% to 4.75%.

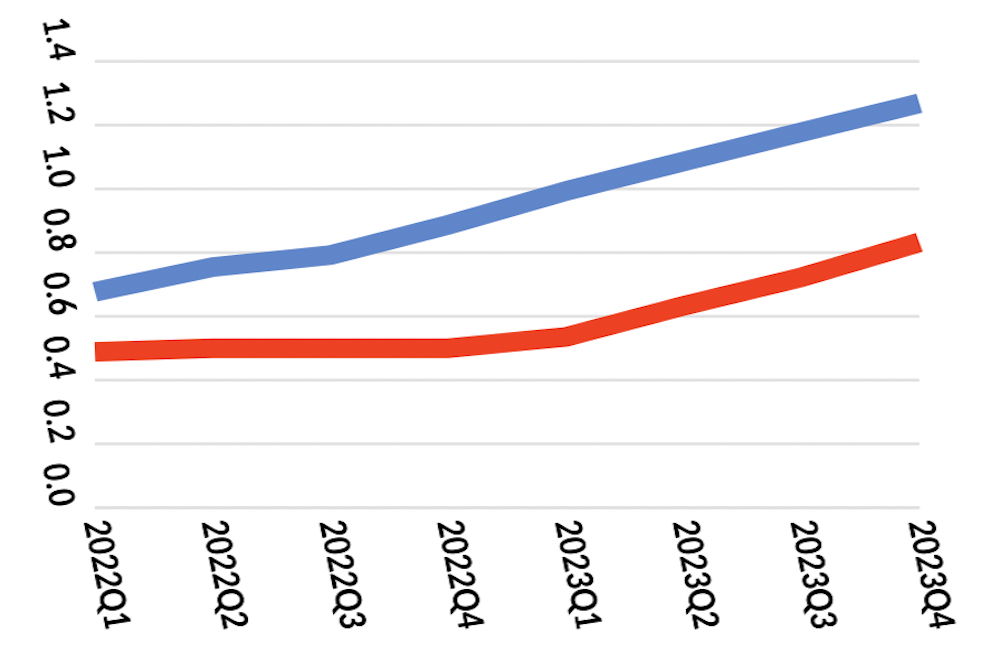

For this reason, the chart below shows both the policy tool’s interest rate predictions over the next couple of years in blue, and an alternative scenario in red in which each element of the aggregate risk index has a 25% weighting. Interestingly, the alternative scenario predicts that the MPC leaves interest rates unchanged at the upcoming meeting and is even more dovish in 2022 and 2023 than in my main prediction. This is because a higher weight on the (rising) geopolitical risk counteracts, to a large extent, interest rate rises due to rising inflation because it implies more damage to growth.

BoE interest rate predictions 2022-23 (%)

Author provided

My policy tool assumes that inflation remains as high as 3.1% in the first quarter of 2024 – significantly higher[23] than the 2.15% forecast made by the Bank of England prior to the Ukraine invasion. It also assumes that inflation reverts back to the 2% target by the end of 2024.

The tool also assumes a negative effect on UK economic growth: 1 percentage point less than its potential growth in the second and third quarters. This is from raised energy prices, the government’s decision to phase out[24] Russian oil imports by the end of 2022 and general elevated uncertainty related to the war. (It is worth noting that the UK gets around 4%[25] of its gas and around 11%[26] of its oil from Russia.)

As far as the aggregate risk index is concerned, the assumption is that the current crisis does not escalate to a widespread, persistent war. I’m assuming that the index rises to 0.35 in mid-2022 before reverting to zero by the end of 2023.

What happens next

Based on these assumptions, I expect that the MPC’s latest meeting will increase UK interest rates, in line with market expectations, to close to 0.75%. But it will then raise them to just 1.3% by the end of 2023 – considerably less than what financial markets predict. And though I don’t project US rates in the same way, it might be reasonable to expect decisions from the Fed to follow a similar trajectory.

As far as the UK is concerned, different assumptions of the policy tool obviously lead to different interest rate predictions. For example, some might argue that my 10% weighting for geopolitical risk in the total aggregate risk calculation is too low. After all, in 2001 the MPC responded to the 9/11 attacks by holding a special meeting[27] in which it cut the policy rate from 5% to 4.75%.

For this reason, the chart below shows both the policy tool’s interest rate predictions over the next couple of years in blue, and an alternative scenario in red in which each element of the aggregate risk index has a 25% weighting. Interestingly, the alternative scenario predicts that the MPC leaves interest rates unchanged at the upcoming meeting and is even more dovish in 2022 and 2023 than in my main prediction. This is because a higher weight on the (rising) geopolitical risk counteracts, to a large extent, interest rate rises due to rising inflation because it implies more damage to growth.

BoE interest rate predictions 2022-23 (%)

Author provided

Other outcomes are also possible. If, for instance, the ongoing crisis escalates much further, energy price pressures will push inflation well in excess of 3% two years into the future. Yet the risk index would also rise as a result, and UK growth would take a further hit. In such a situation, the Bank of England would face an acute stagflation dilemma. That would make interest rate decisions even harder to predict, since a big hit to UK growth would open the door to interest rate cuts – and potentially more QE.

References^ the bottlenecks (www.theguardian.com)^ global economic damage (www.bbc.co.uk)^ to reach 0.5% (tradingeconomics.com)^ quantitative easing (QE) programme (www.bloomberg.com)^ currently stands (www.ons.gov.uk)^ it is expected (www.theguardian.com)^ even higher (think.ing.com)^ already nudging 8% (www.theguardian.com)^ currently expect (www.ft.com)^ en route to (www.bankofengland.co.uk)^ heading towards 2% (www.cnbc.com)^ consistently overestimated (blogs.lse.ac.uk)^ Dan Brown (www.goodreads.com)^ monetary policy tool (theconversation.com)^ inflation forecast (www.bankofengland.co.uk)^ Office for Budgetary Responsibility (OBR) data (obr.uk)^ bad for economic growth (papers.ssrn.com)^ can delay (www.sciencedirect.com)^ economic policy uncertainty (www.policyuncertainty.com)^ financial stress (sdw.ecb.europa.eu)^ infectious diseases (www.policyuncertainty.com)^ global geopolitical risk (www.matteoiacoviello.com)^ significantly higher (www.bankofengland.co.uk)^ phase out (www.reuters.com)^ gets around 4% (www.gov.uk)^ around 11% (www.iea.org)^ special meeting (www.bankofengland.co.uk)

Author provided

Other outcomes are also possible. If, for instance, the ongoing crisis escalates much further, energy price pressures will push inflation well in excess of 3% two years into the future. Yet the risk index would also rise as a result, and UK growth would take a further hit. In such a situation, the Bank of England would face an acute stagflation dilemma. That would make interest rate decisions even harder to predict, since a big hit to UK growth would open the door to interest rate cuts – and potentially more QE.

References^ the bottlenecks (www.theguardian.com)^ global economic damage (www.bbc.co.uk)^ to reach 0.5% (tradingeconomics.com)^ quantitative easing (QE) programme (www.bloomberg.com)^ currently stands (www.ons.gov.uk)^ it is expected (www.theguardian.com)^ even higher (think.ing.com)^ already nudging 8% (www.theguardian.com)^ currently expect (www.ft.com)^ en route to (www.bankofengland.co.uk)^ heading towards 2% (www.cnbc.com)^ consistently overestimated (blogs.lse.ac.uk)^ Dan Brown (www.goodreads.com)^ monetary policy tool (theconversation.com)^ inflation forecast (www.bankofengland.co.uk)^ Office for Budgetary Responsibility (OBR) data (obr.uk)^ bad for economic growth (papers.ssrn.com)^ can delay (www.sciencedirect.com)^ economic policy uncertainty (www.policyuncertainty.com)^ financial stress (sdw.ecb.europa.eu)^ infectious diseases (www.policyuncertainty.com)^ global geopolitical risk (www.matteoiacoviello.com)^ significantly higher (www.bankofengland.co.uk)^ phase out (www.reuters.com)^ gets around 4% (www.gov.uk)^ around 11% (www.iea.org)^ special meeting (www.bankofengland.co.uk)