How 'drinkflation' affects the price of your pint

- Written by: Colin Angus, Senior Research Fellow in the Sheffield Alcohol Research Group, University of Sheffield

The cost of living crisis has seen the prices of many goods and services rise sharply in the past 18 months, but food and drink prices have been particularly hard hit.

Some food producers have responded by reducing the size of their products, while keeping prices the same – a phenomenon known as “shrinkflation[1]”.

When several major brewers were reported to have reduced the strength of beers recently, including Fosters lager (cut from 4% alcohol by volume (ABV) to to 3.7%) and ales such as Old Speckled Hen and Spitfire, it led to accusations of “drinkflation”[2] and short-changing of customers.

Duty on beer is levied on the basis of alcohol content, so a 0.3% reduction in ABV equates to a saving of around 4p on a pint. Brewers can pocket this if they keep the sales price the same. If this seems like small beer, consider the fact that we drink around 7.8 billion pints[3] each year in the UK, meaning that a 0.3% cut across all beers would see industry revenue rise by £290 million a year.

Brewers and the British Beer and Pub Association have pointed to rising production costs[4] and squeezed profit margins as the justification for these reductions in strength. But concerns remain that the great British pint is becoming another casualty of the cost of living crisis.

But this is not a new phenomenon. Brewers have been cutting the strength of major beer brands for well over a decade[5]. In many cases this is done with minimal publicity and without many consumers even noticing.

HMRC collects alcohol taxes[6] on behalf of the UK Treasury and requires all alcoholic products above 1.2% to advertise their alcoholic strength on the label. But beer producers are allowed a little wiggle room[7] around this, provided the value on the label is within 0.5% of the true strength.

This is a concession to small producers who may find it hard to produce every batch to exactly the same ABV but don’t want to have to produce new labels with each small variation.

Molson Coors took advantage of this leeway in 2012 to reduce the strength of Carling[8] from 4% to 3.7%, but continued to label and market it as 4%. This only came to light when HMRC took the company to court[9] for paying duty at the lower rate. Ultimately Carling won the court case, but this calls the strength of the contents of your can or pint glass into question.

It is also important to point out that long-term trends in alcohol consumption have not favoured beer producers and so they may be looking for ways to recover lost revenues. In 1970, UK adults drank an average of 181 pints of beer per year. By 2021 that had fallen to 120. Over the same period, average wine consumption increased from 5 to 28 bottles per year.

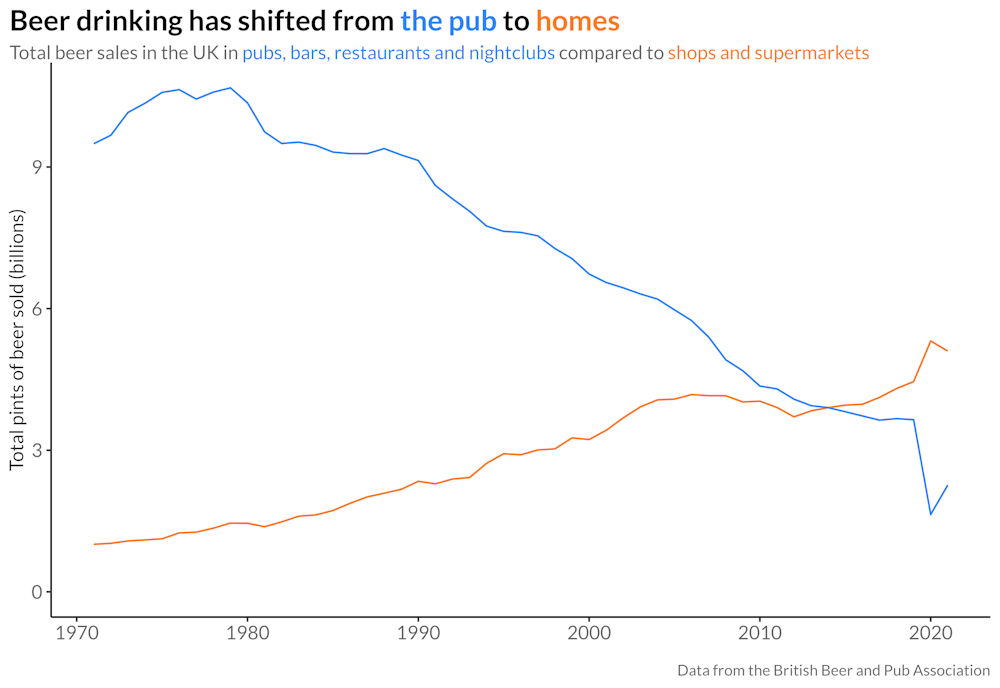

These changes in drinking patterns have run alongside a gradual shift away from drinking in the pub to drinking at home. A couple of decades ago we drank two-thirds of our beer in pubs and bars, according to data from the British Beer and Pub Association – today it’s less then one-third.

COVID lockdowns and the closure of pubs for much of the pandemic has only served to accelerate these trends, as has an ever-widening gap[10] in the price of drinks in the pub compared to the supermarket.

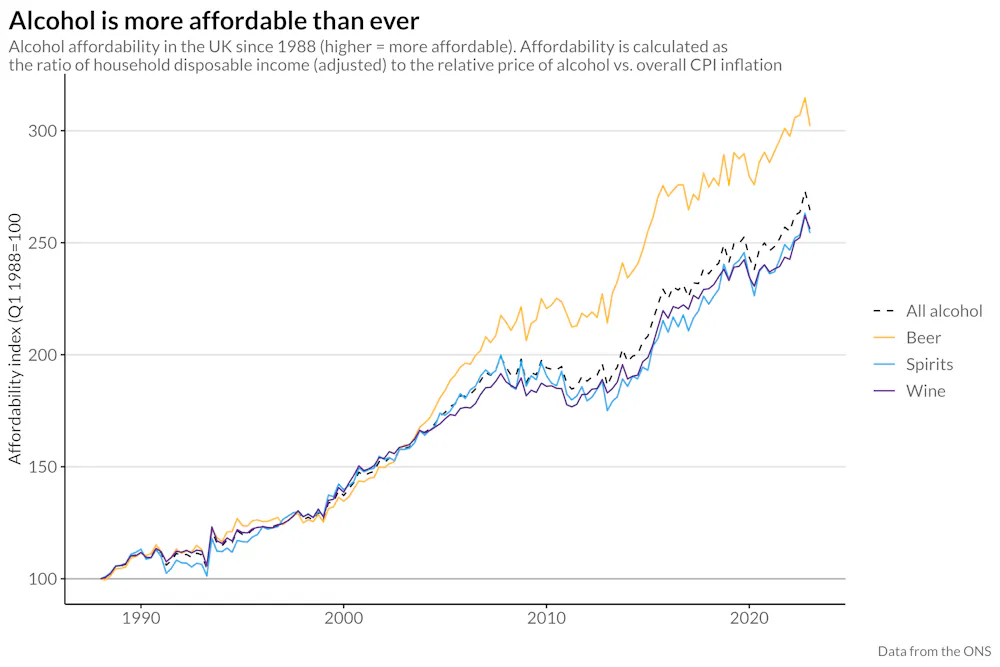

Data from ONS, analysis by Colin Angus, Author provided[15]

All of this means that it’s little surprise to see brewers looking for ways to increase their profits. Making small reductions in alcoholic strength is one way they can do this.

But are consumers being cheated? People’s perspective on this will depend on their motivations for drinking beer. With shrinkflation, consumers are paying the same amount for a chocolate bar or a bag of crisps, but getting less. With “drinkflation” consumers are still getting the same amount of beer, it just contains slightly less alcohol.

So, only people who are drinking for the specific purpose of getting drunk are being “short-changed”. For people who are drinking beer because they like the taste, or who see beer as an important part of a social ritual, the lower alcohol content is more likely to be a positive, given that people consume less alcohol[16] when drinking lower strength beer and the health benefits of reduced alcohol intake.

In line with this, the low alcohol and alcohol-free beer industry[17] is growing. Most shops and many bars now offer at least one alcohol-free beer option. The UK market has also seen the launch of several lower-strength, carb and calorie versions of existing brands, such as Heineken Silver[18].

Data from ONS, analysis by Colin Angus, Author provided[15]

All of this means that it’s little surprise to see brewers looking for ways to increase their profits. Making small reductions in alcoholic strength is one way they can do this.

But are consumers being cheated? People’s perspective on this will depend on their motivations for drinking beer. With shrinkflation, consumers are paying the same amount for a chocolate bar or a bag of crisps, but getting less. With “drinkflation” consumers are still getting the same amount of beer, it just contains slightly less alcohol.

So, only people who are drinking for the specific purpose of getting drunk are being “short-changed”. For people who are drinking beer because they like the taste, or who see beer as an important part of a social ritual, the lower alcohol content is more likely to be a positive, given that people consume less alcohol[16] when drinking lower strength beer and the health benefits of reduced alcohol intake.

In line with this, the low alcohol and alcohol-free beer industry[17] is growing. Most shops and many bars now offer at least one alcohol-free beer option. The UK market has also seen the launch of several lower-strength, carb and calorie versions of existing brands, such as Heineken Silver[18].

Read more https://theconversation.com/how-drinkflation-affects-the-price-of-your-pint-209167