why the housing market is collapsing – and the risks to the wider economy

- Written by Zhirong Ou, Senior Lecturer in Economics, Cardiff Business School, Cardiff University

China has been trimming interest rates[1] recently – in contrast to other[2] major[3] economies[4] – as it tries to stem the economic effects of its zero-COVID policy and address a growing property crisis. The country’s traditionally strong housing market has been affected by a funding crisis that has seen development paused and led to buyers refusing to pay their mortgages.

The recent spate of mortgage strikes by homebuyers across China has exposed the risk that has accumulated in the market as it has developed over the past two decades. The mortgage strikes started earlier this year among a group of people that bought homes in an Evergrande development in Jingdezhen city, Jiangxi province, but protests have since spread to buyers of other developments throughout China.

To date, more than 300[5] groups of homeowners are believed to be refusing to pay between US$150 billion (£127 billion) and US$370 billion[6] in homeloans, according to informal surveys published online.

These protesters all have one thing in common: they have been paying mortgages, often at a rate of 5%-6%, on homes they have never lived in. These properties were sold before they were built under what’s called the presale system, which is a common way[7] to buy property in China.

The trigger for the buyers’ strikes is a widespread belief among these protesters that the funds homeowners have paid in advance to the builders of these property developments have been misused.

Under the presale system, buyers deposit money in an account before the property is built. Chinese banks and local authorities are obligated to monitor developers’ use of these funds. Developers are not supposed to have access to all of the money until they have hit certain pre-agreed milestones during the building process.

But buyers have recently complained[8] that many banks –- whether or not local authorities are aware is unclear –- have been providing loans to developers before the required stage[9] of work has been reached.

Buyers have also complained that, although these funds should have been kept in designated escrow accounts that regulators can monitor, sometimes they are not, enabling developers to evade regulations[10]. Overall, these buyers believe loose regulation of funds has provided some developers with both the temptation and ability to keep investing in new projects, by borrowing more before current projects are completed.

Indeed, a commonly observed pattern[11] in China’s property development industry is for developers to purchase lands, pledge them to banks to get loans, start projects, begin the presale process with buyers and then use these funds to purchase lands for other projects.

In such situations, only a portion of a buyer’s funds might go towards the construction of their own property. As a result, a recent liquidity crisis in the sector has stalled many projects because the developers involved can’t afford to continue building.

The rise and fall of the Chinese property market

Today’s situation follows a boom in the Chinese property market[12]. The housing market had been enjoying a long rise since the early 2000s, which reached a peak in 2018 before a gradual cooling that ended in a sharp decline in sales in early 2022.

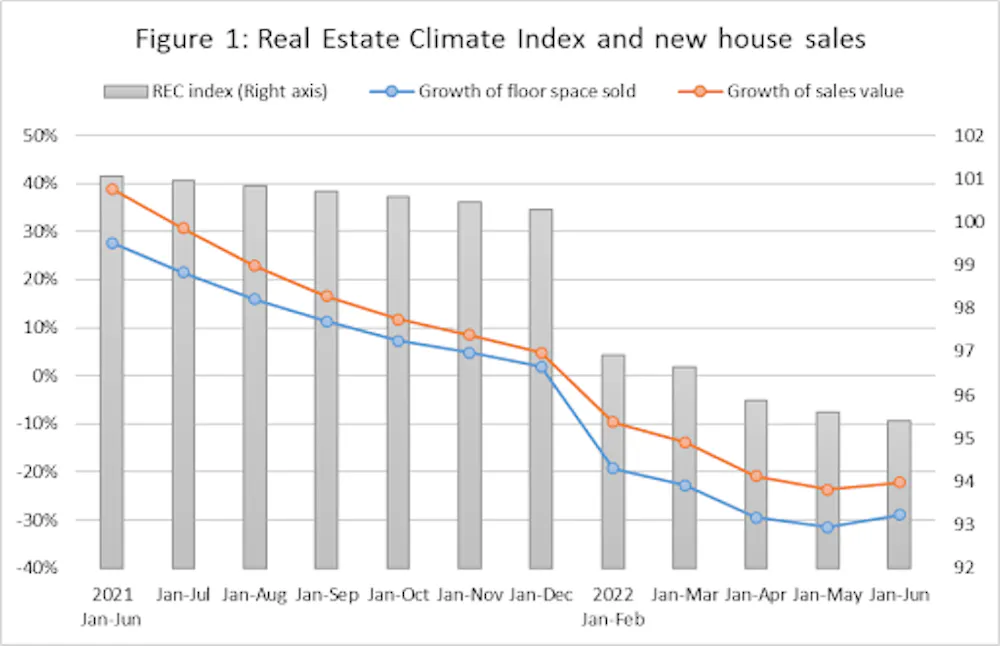

The chart below (figure 1) shows the change in China’s Real Estate Climate index, which measures aggregate business activity in land sales and real estate. New house sales have slumped substantially this year, with values dropping by 22% compared to the same time last year.

Author's chart based on figures from National Bureau of Statistics of China[14]

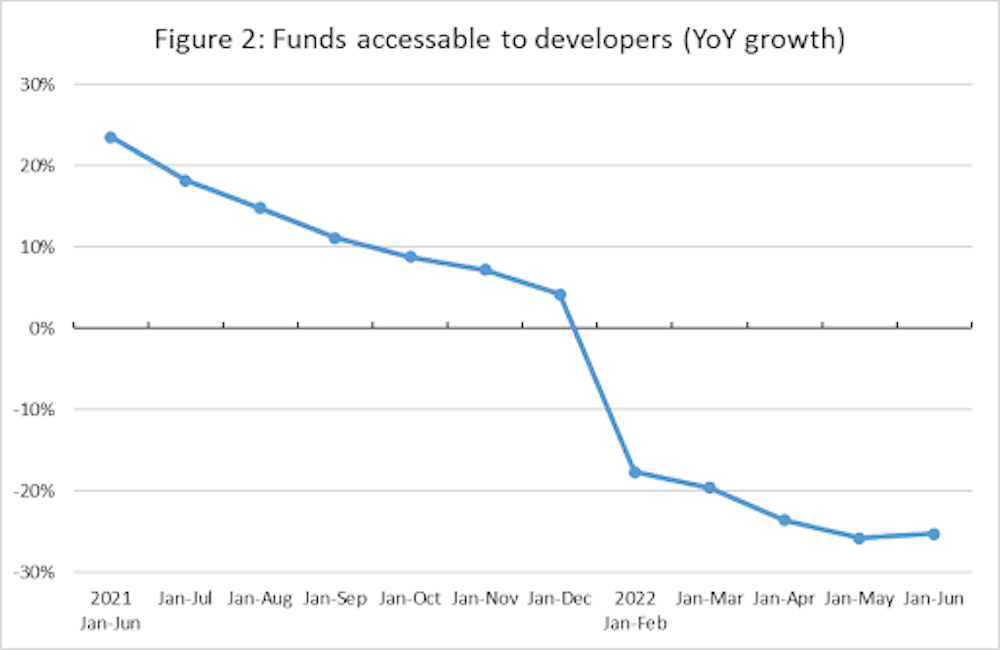

Tightening credit conditions also play an important role. Among other things, a key policy change is the government’s “three red lines”[15] regulation, introduced[16] in August 2020. It categorises developers according to how much debt they hold, which then determines how much more they can borrow annually.

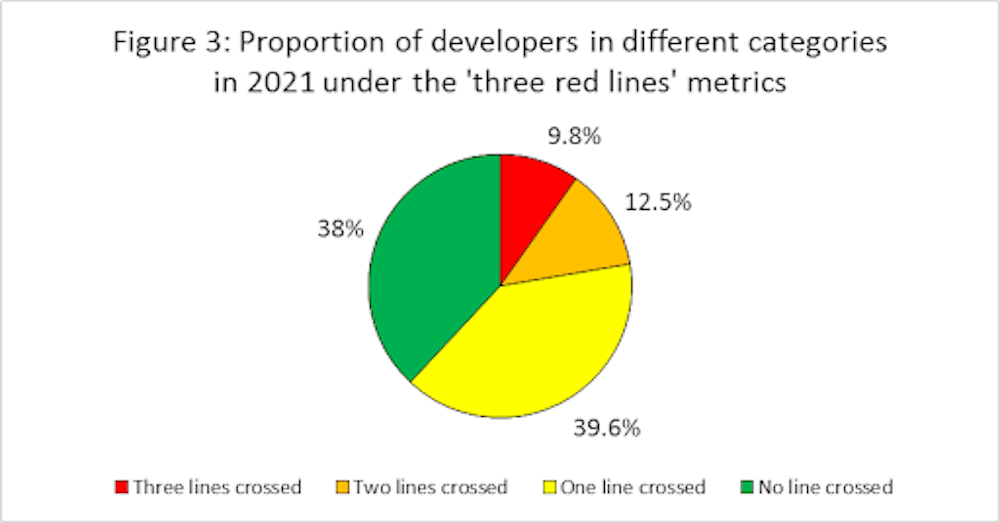

More than 60% of developers have hit at least one of the debt thresholds set by regulators in 2021, as shown in figure 3 below. Around 10% – crisis-hit Evergrande[17] included – have breached all three. When this happens, developers are not allowed to raise new borrowing for that year. The resulting credit crunch has pushed many developers into a stressed position, with some even defaulting.

Author's chart based on figures from National Bureau of Statistics of China[14]

Tightening credit conditions also play an important role. Among other things, a key policy change is the government’s “three red lines”[15] regulation, introduced[16] in August 2020. It categorises developers according to how much debt they hold, which then determines how much more they can borrow annually.

More than 60% of developers have hit at least one of the debt thresholds set by regulators in 2021, as shown in figure 3 below. Around 10% – crisis-hit Evergrande[17] included – have breached all three. When this happens, developers are not allowed to raise new borrowing for that year. The resulting credit crunch has pushed many developers into a stressed position, with some even defaulting.

Red: no new interest-bearing debt is allowed. Orange: new interest-bearing debt growth must not exceed 5%. Yellow: new interest-bearing debt growth must not exceed 10%. Green: new interest-bearing debt growth must not exceed 15%.

Author's chart based on reports from China Real Estate Data Academy.[18]

The wider effects

The potential for a wave of developer bankruptcies is the biggest risk to China’s housing market at the moment and could result in a large number of unfinished properties.

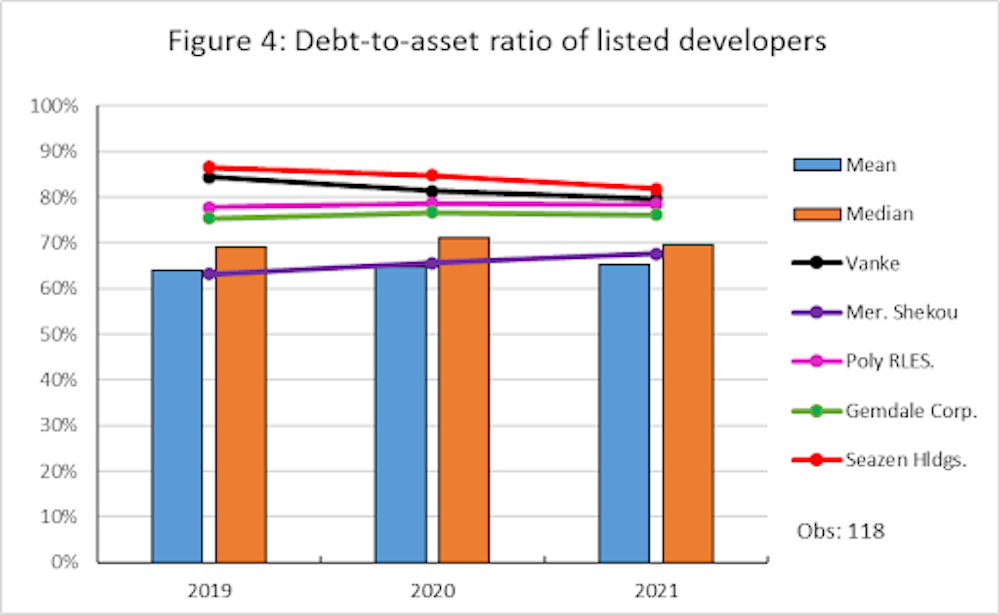

This is not alarmism: Chinese developers generally borrow a lot of money to fund ongoing construction. While the industry average debt-to-asset ratio is around 65%, some of the leading companies are even more indebted (see figure 4 below).

Red: no new interest-bearing debt is allowed. Orange: new interest-bearing debt growth must not exceed 5%. Yellow: new interest-bearing debt growth must not exceed 10%. Green: new interest-bearing debt growth must not exceed 15%.

Author's chart based on reports from China Real Estate Data Academy.[18]

The wider effects

The potential for a wave of developer bankruptcies is the biggest risk to China’s housing market at the moment and could result in a large number of unfinished properties.

This is not alarmism: Chinese developers generally borrow a lot of money to fund ongoing construction. While the industry average debt-to-asset ratio is around 65%, some of the leading companies are even more indebted (see figure 4 below).

Author's chart based on figures from China Stock Market & Accounting Research (CSMAR) Database.[19]

The industry has also seen a gradual fall in developers’ current ratios (their ability to repay short-term debts, see figure 5 below), which indicates lower overall liquidity and leaves the industry vulnerable to financial shocks.

Author's chart based on figures from China Stock Market & Accounting Research (CSMAR) Database.[19]

The industry has also seen a gradual fall in developers’ current ratios (their ability to repay short-term debts, see figure 5 below), which indicates lower overall liquidity and leaves the industry vulnerable to financial shocks.