what the Bank of England's historic hike means for your money

- Written by: Jonquil Lowe, Senior Lecturer in Economics and Personal Finance, The Open University

The Bank of England has raised its base rate by 0.5 percentage points, the largest single upward jump in 27 years. It takes the base rate to 1.75%, its highest level since 2008. This latest interest rate hike will affect personal finances and reflects the Bank’s efforts to control rampant inflation[1] amid the cost of living crisis[2] in the UK.

The government tasked the Bank of England with maintaining UK inflation at a stable level of 2% a year[3]. At present, inflation is way above this target at 9.4%[4], and it’s currently forecast to reach 13%[5] by October. Among the main reasons[6] for this high inflation is the massive surge in the prices of global energy, grain and other key commodities. This has been caused by recent supply chain disruption and the Russian war on Ukraine.

Read more: Five essential commodities that will be hit by war in Ukraine[7]

These external factors are beyond the Bank of England’s control. But the Bank is concerned that high levels of inflation will become baked into the economy if domestic wages and prices spiral upwards to compensate for these global price rises. By raising the base rate, it aims to slow the UK economy, weakening workers’ wage bargaining power and so forcing inflation back down.

This isn’t going to happen overnight. It takes one to two years[8] for the effects of base rate increases to work through the economy. But once this happens, the effects are painful. The Bank has forecast that unemployment will rise from 3.8% today[9] to 5.5% next year[10], implying that an extra 600,000 people will lose their jobs. And, if your wages and other income are lagging behind inflation, your standard of living is being squeezed.

The Bank of England base rate is an important benchmark used by banks to set the interest rates for all kinds of financial products. So, when it comes to personal finances, a base rate rise has a varied impact. Here are the main ways your money will be affected.

Your savings

In theory, the rise in the Bank of England base rate should be good news for savers with bank and building society accounts and government-backed National Savings & Investment[11] products. The rise should be passed on to your account’s interest rate, although this depends on the extent to which providers allow their savings rates to follow the rise in base rates, as well as how far rates actually rise.

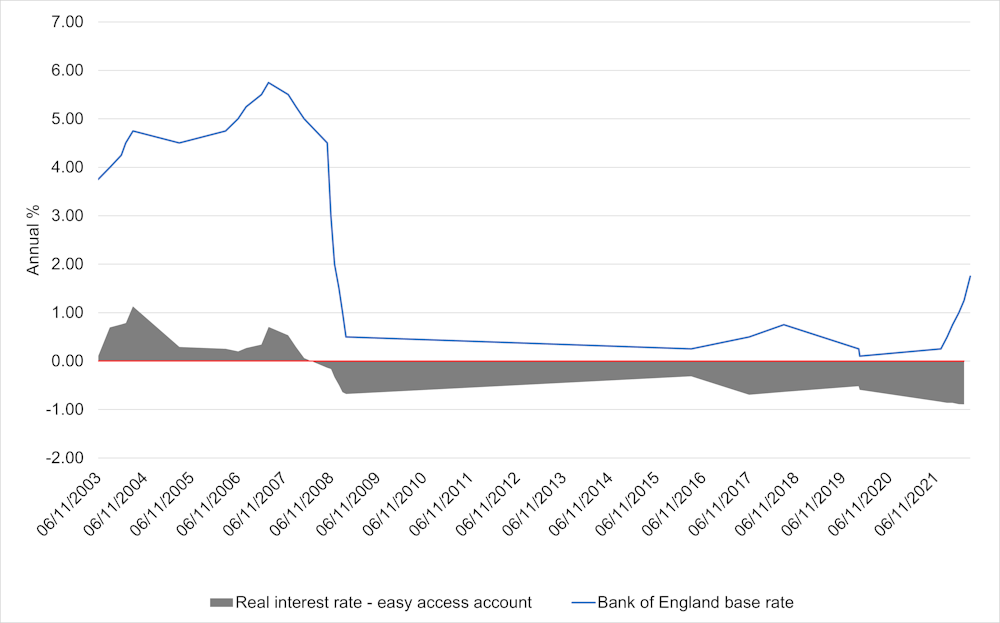

Savers should look at the real return, which is the quoted interest rate less the inflation rate. As the chart below shows, easy-access savers last saw inflation-beating returns back in early 2008, before the global financial crisis took hold. Since then, real returns have been persistently negative. In effect, this means savers are paying for the privilege of keeping their money readily accessible.

Bank of England base rate versus savings rates

Back in November 2021, before this recent series of base rate rises, the best easy-access accounts were offering rates of around 0.60% to 0.70% a year, according to my research using Moneyfacts[12] data. By June, these rates had risen to 1.55% but this has been outstripped by the rise in inflation and so savers’ real returns have fallen rather than improved.

Rates are higher – at more than 3% a year – if you’re prepared to lock your money away for two to five years. That could look appealing if you expect a fairly rapid fall in inflation back to the 2% target.

Your pension

When approaching retirement, you may use some or all of your pension savings to buy an annuity[13]. Although this is a product that pays a secure income for life, you must give up your savings to buy it and changing your mind later on is not an option.

The rising base rate is feeding through to improve annuity rates. For example, if you’re 65 years old, with an average pot size of £68,000[14], Moneyfacts[15] data suggests you could have bought a fixed yearly income for life of £3,352 in November 2021. By June, that potential income increased by more than a fifth to £4,066.

Your mortgage

House prices have boomed for decades, especially since the 2008 global financial crisis. This has been fuelled by central bank quantitative easing[16] programmes, which are designed to drive down interest rates and cause asset prices to rise because more money is available for borrowing and investing.

Rising house prices have been a boon if you’re already a homeowner, but this has also made it increasingly difficult for new buyers to afford a home. The average house price was around four times[17] average earnings at the start of this century, rising to seven times by 2007 and is now eight times earnings. This means newer buyers have to take on much larger mortgage debts than previous generations.

Large mortgages were not a problem while interest rates were historically low, as they have been since 2008. But the rise in base rates is now storing up problems in this area. Around three-quarters of current mortgage borrowers are on a fixed-rate deal[19] of two to five years. If that applies to you, you’re sheltered from the base rate rises for now, but you should prepare for a jump in your repayments when your fixed-rate deal comes to an end. For the 2 million borrowers with a standard variable rate or tracker mortgage, housing costs are already rising rapidly.

Another important consideration is whether rising mortgage costs will choke demand and cause house prices to fall. The Halifax House Price Index[20] shows no sign of a slowdown yet, which it attributes to a persistent supply shortage and continuing demand from better-off households who accumulated savings during the pandemic.

On the other hand, another major UK house price tracker, the Nationwide House Price Index, is showing “tentative signs of a slowdown in activity”. This has yet to feed through to prices. But the building society’s chief economist expects the UK housing market to slow as inflation puts pressure on household budgets and as the Bank of England raises interest rates further. As he points out, this is “widely expected[21]” to happen.

References

- ^ rampant inflation (www.theguardian.com)

- ^ cost of living crisis (www.theguardian.com)

- ^ 2% a year (www.bankofengland.co.uk)

- ^ 9.4% (www.ons.gov.uk)

- ^ reach 13% (www.bankofengland.co.uk)

- ^ main reasons (www.bankofengland.co.uk)

- ^ Five essential commodities that will be hit by war in Ukraine (theconversation.com)

- ^ one to two years (www.bankofengland.co.uk)

- ^ 3.8% today (www.ons.gov.uk)

- ^ 5.5% next year (www.bankofengland.co.uk)

- ^ National Savings & Investment (www.nsandi.com)

- ^ Moneyfacts (www.moneyfactsgroup.co.uk)

- ^ buy an annuity (www.unbiased.co.uk)

- ^ average pot size of £68,000 (www.fca.org.uk)

- ^ Moneyfacts (www.moneyfactsgroup.co.uk)

- ^ quantitative easing (www.bankofengland.co.uk)

- ^ four times (www.ons.gov.uk)

- ^ khz / Shutterstock (www.shutterstock.com)

- ^ fixed-rate deal (www.ukfinance.org.uk)

- ^ Halifax House Price Index (www.halifax.co.uk)

- ^ widely expected (www.nationwidehousepriceindex.co.uk)