Raising UK state pension age to 66 has seen big increase in working 65-year-olds, but particularly deprived women

- Written by: Laurence O'Brien, Research Economist, Institute for Fiscal Studies

The UK state pension age has been rising in recent years, most recently with a staggered increase[1] for both men and women from 65 to 66 between December 2018 and October 2020. While the male state pension age had previously been 65 since the late 1940s, for women this followed a previous rise in their state pension age from 60 to 65 between 2010 and 2018.

Further increases have been legislated, starting with an increase for both men and women from 66 to 67 scheduled between 2026 and 2028, as the government attempts to counteract some of the pressures to the national finances brought on by an ageing population. The government also recently launched the second independent review[2] of the state pension age, to be published in May 2023, among whose questions is to consider whether to bring forward by eight years plans to raise the age to 68 by 2046.

But how are these increases to the state pension age likely to affect the labour market? In an ongoing programme of work[3] at the Institute for Fiscal Studies, funded by the Centre for Ageing Better[4], we have examined in detail the effect of the recent increase in the state pension age from 65 to 66 on economic activity.

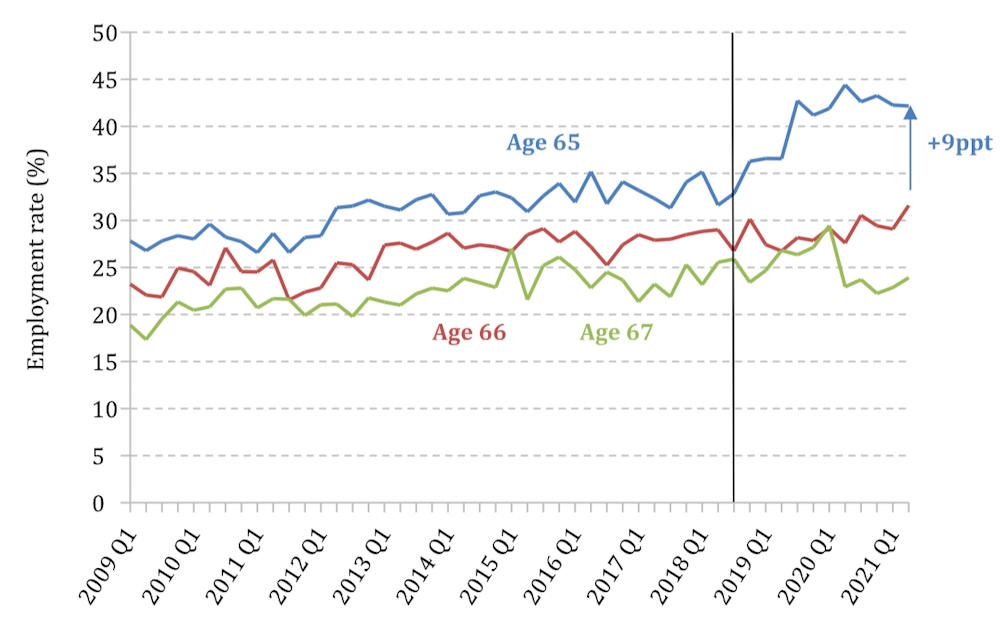

The reform increased employment significantly among older workers. As you can see from the two charts below, it led to a marked increase in the share of 65-year-olds in paid work. We can see that, between late 2018 and late 2020, the employment rates of 65-year-old men and women jumped up by around ten percentage points each. This was not matched by a similarly large increase in the employment rates of 66 and 67-year-olds, indicating that the state pension age rise was driving this.

Employment rates of men aged 65-67

Employment rates of women aged 65-67

The black vertical line shows the last quarter in which all 65-year-olds were over the state pension age (2018Q3); ppt = percentage point.

The black vertical line shows the last quarter in which all 65-year-olds were over the state pension age (2018Q3); ppt = percentage point.

Overall, we estimate that the increase in the state pension age led to an additional 7% of men and 9% of women staying in paid work at age 65 – this translates to around 55,000 extra 65-year-olds in paid work. By mid-2021, the male employment rate at age 65 had risen to 42% (from 35%) and the female rate to 31% (from 22%).

Both are the highest seen since at least the mid-1970s and, at least in the case of women, very likely to be the highest rate ever in the UK. But, despite this increase, it still means that the majority of men and women are not in paid work before they reach the state pension age of 66. However, employment rates at these older ages vary along several characteristics, so it’s important to analyse how different groups responded to the state pension age rise.

Unequal employment effects

In the most deprived 20% of areas, women’s employment rate at the age of 65 rose by 13 percentage points and men’s by ten percentage points. In contrast, in the most prosperous areas, female and male employment rates at age 65 rose by just four and five percentage points respectively. These results suggest that less-advantaged people are more likely to continue to work as a result of the higher state pension age, probably because many of them cannot afford to retire without state pension income.

It is true that most of those who continue in paid work due to the reform are likely to be financially better off by doing so, because their extra earnings are likely to outweigh their lost pension income. We find that most of the increase in paid work is full-time work, despite the fact that 20 hours a week of employment at the UK adult minimum wage (National Living Wage) of £8.91 per hour would be sufficient to make up for the loss of a full new state pension.

But while financially better off, this is not to say that many of these workers would not have preferred to have been able to retire earlier and enjoy more leisure time. Delaying retirement may be difficult and disruptive for many, so the government should prioritise clear communication of changes to people’s state pension ages well in advance – especially to less-advantaged groups whose retirement plans may be more affected by the changes, and who have been found to be[5] less aware of past state pension age reforms.

Not everyone changed retirement plans

Despite the large employment effects, it remains the case that more than 90% of 65-year-olds (around 640,000 of them) have not changed whether they are in paid work at age 65 purely because of the higher state pension age. This is in large part because the majority of men and women have already left the labour market before their 65th birthday, while some others would have remained in paid work even if the state pension age had remained at 65.

A group that faces obvious difficulties as a result of the higher state pension age are those who would like to work but cannot, perhaps because they can’t find a job, or because of health problems. We find that the higher state pension age led to 5,000 extra unemployed 65-year-olds and an additional 25,000 65-year-olds who report that they cannot work due to poor health.

Given the lower generosity of the working-age benefit system compared to the state pension, this group will be of particular concern for policymakers. In particular, ensuring that older jobseekers are sufficiently supported – for example, by ensuring that Jobcentre staff are attuned to their needs and challenges – to find appropriate work becomes ever more important as the state pension age rises.

References

- ^ staggered increase (assets.publishing.service.gov.uk)

- ^ second independent review (www.cipp.org.uk)

- ^ ongoing programme of work (ifs.org.uk)

- ^ Centre for Ageing Better (ageing-better.org.uk)

- ^ have been found to be (ifs.org.uk)