What's wrong with Australian mortgages? They're fixed for shareholders, not home owners

- Written by: Richard Holden, Professor of Economics, UNSW

If you’re paying off a mortgage – or aspiring to – imagine if you didn’t have to worry so much about rising interest rates.

That’s already the reality for US home buyers. Unlike in Australia, most mortgages in the US have a fixed-interest rate, locked in for 30 years.

Instead of having to wait and see if their central bank (the Federal Reserve) raises rates each month, a US 30-year fixed mortgage at 2% will still have the same monthly repayment – even after a rate rise.

In contrast, when the Reserve Bank of Australia lifts rates it has huge implications for household budgets, because most borrowers still have variable-rate mortgages.

Every time the cash rate increases and banks inevitably pass through that increase, our mortgage payments go up too – adding thousands of dollars to average annual repayments.

This is one reason why RBA governor Philip Lowe has been so cautious[1] about following the US Federal Reserve’s strong signal about lifting interest rates.

So why don’t Australian lenders offer 30-year fixed-rate mortgages too, like their US counterparts?

Every extra 1% can cost thousands

Here in Australia, an extra 1% on a A$600,000 mortgage means $6,000 a year more in interest payments. And these are post-tax dollars. So if you earn $100,000 and hence pay an average tax rate of 25%, that’s like taking a roughly $8,000 pay cut. Ouch.

A 3% rise in official rates over two to three years is not impossible. On a $600,000 mortgage that would mean an extra $18,000 a year in interest payments.

The RBA knows this, of course. It looks at Australian household debt of more than 120% of GDP and knows raising rates too aggressively risks putting a significant number of Australian households into financial distress.

Read more: Top economists expect RBA to hold rates low in 2022 as real wages fall[2]

In one sense this is good news. It means the RBA has large-calibre ammunition to fire in pursuit of its monetary policy goals (to keep unemployment low and inflation between 2% and 3%).

But it would be better if the Australian mortgage market involved less risk for consumers.

There is no reason why Australian lenders couldn’t offer 30-year fixed-rate mortgages. After all, there’s an active government bond market with maturities from one year to 30 years. This provides a benchmark to price mortgages.

Two fixes for more affordable mortgages

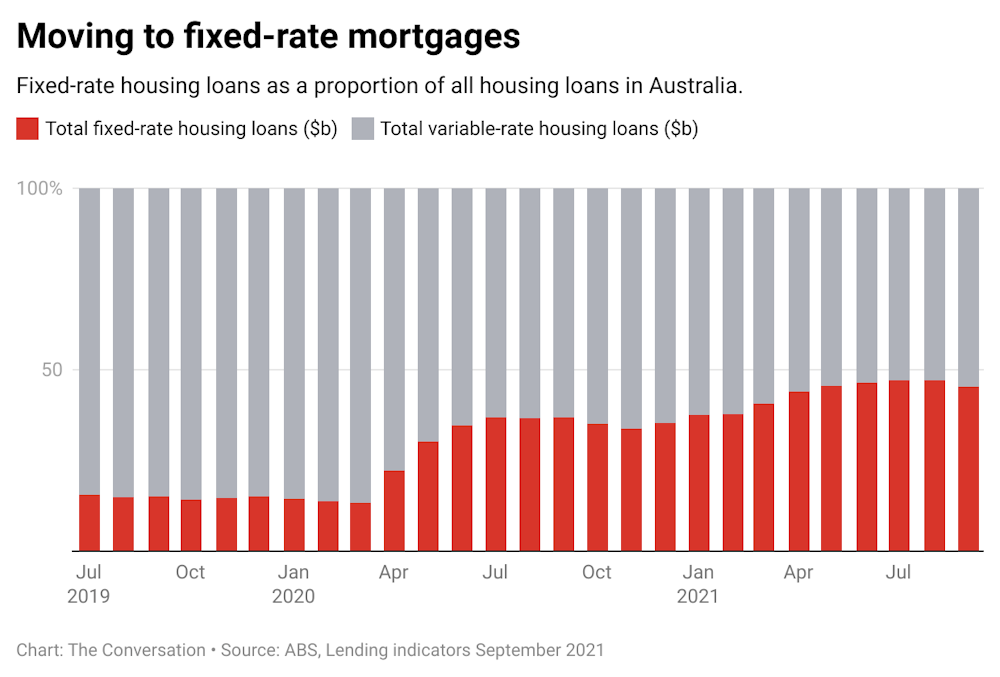

Fixed-rate mortgages have become much more popular in Australia in the past few years: the proportion of new mortgages that were fixed jumped from about 15% in June 2019 to more than 45% by September 2021.