Interest rates have stopped rising, but 2023 hikes could still cause recession for some economies

- Written by: Alan Shipman, Senior Lecturer in Economics, The Open University

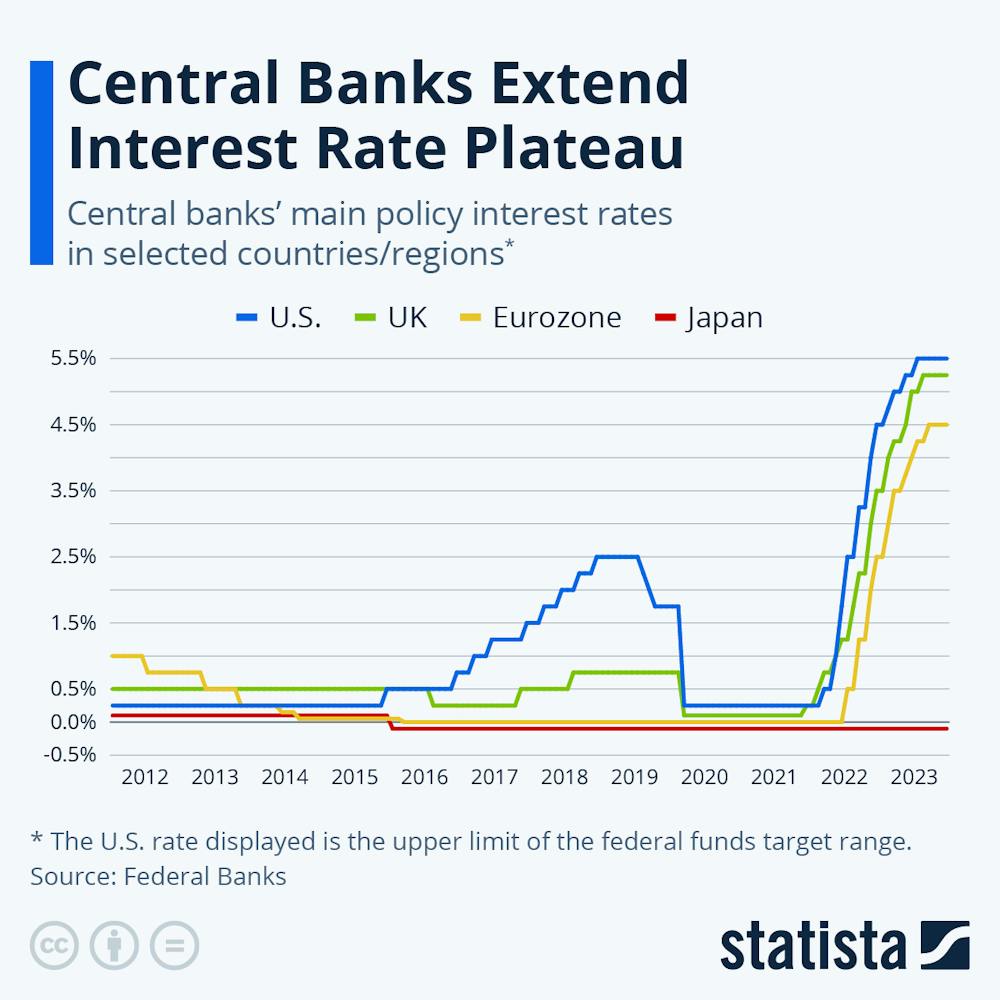

Central banks on both sides of the Atlantic kept their main interest rates unchanged for the fourth successive month in December 2023. These rates are closely watched because they set the minimum interest at which your bank borrows and lends. This determines the cost of credit for all firms and households with mortgages or other loans.

The European Central Bank (ECB), the US Federal Reserve and the UK Bank of England have raised interest rates sharply since the start of 2022. This was in response to a surge in inflation – the annual increase in consumer prices – far above the 2% rate that all these central banks now target.

But UK inflation is taking longer to respond than that of the US or EU. This has renewed debate over whether rate cuts are the best or only way[1] to keep inflation under control. It has also caused a shift in opinions about which western economies are most at risk of recession in 2024.

Read more: Is the UK in a recession? How central banks decide and why it's so hard to call it[2]

Higher interest rates are designed to subdue inflation by reducing the amount people spend. Businesses and households are expected to save more when rates rise, in anticipation of greater interest payments (although that doesn’t always happen[3]). It’s also hoped they’ll borrow less because of the extra interest they would be charged. Those with outstanding loans are left with less to spend on goods and services after paying their interest bill.

Governments are also affected. In the UK, interest on around a quarter of government debt is now linked to inflation[4]. This means more of the budget gets channelled into interest payments, leaving less to spend on public services, when the central bank raises rates.

This restraint doesn’t happen immediately, however. When borrowers take out fixed-rate loans, they aren’t affected by higher base rates until the deal expires. Almost a million UK borrowers, for example, are still on fixed rates of 2% or below that will only come up for renewal[5] – at current, higher rates – in the first quarter of 2024. The resulting delay of a year or more before past interest rate rises kick in makes it hard for central bankers to know when they’ve raised rates enough to cool the economy.

Read more: UK bonds have hit a 25-year high – here's what that means for the economy[6]

Raising interest rates can also restrain inflation by encouraging foreign investors to buy bonds and other financial assets in a country’s currency. The resulting inflow of capital is likely to strengthen its exchange rate. This makes imports cheaper and can help to slow the overall rise in prices.

A stronger currency is especially effective for curbing inflation for economies that consume a high proportion of imports, such as the UK. But it also hurts exporters, and only works if interest rates rise above those of comparable economies. This may be one reason why the Bank of England has raised its interest rates faster and further than the ECB since February 2022.