How to understand what's going on with UK mortgage rates

- Written by: Robert Webb, Professor of Banking & Applied Economics, University of Stirling

The UK mortgage market has tightened as confidence in the economy has faltered in recent weeks. Lenders withdrew more than 1,600 homeloan products[1] after the (then) chancellor Kwasi Kwarteng’s September mini-budget sent the UK economy into a tailspin[2].

Rates on the mortgage products that are still available have risen to record levels – average two-year and five-year fixed rates have now passed 6%[3] for the first time since 2008 and 2010 respectively.

The Bank of England has intervened to try to calm the situation[4]. But this help currently has an end date[5] of Friday 14 October, after which it’s unclear what will happen in the financial markets that influence people’s mortgage rates.

This is a crucial issue for a lot of people: 28% of all dwellings[6] are owned with a loan, with mortgage payments eating up about a sixth of household income[7], on average.

Looking at how the market has developed over time can help to explain how we got here and where we are going – which is basically headfirst into a period of high interest rates, low loan approvals and plateauing house prices.

All financial markets are driven by information, confidence and cash. Investors absorb new information which feeds confidence or drives uncertainty, and then they choose how to invest money. As the economy falters, confidence erodes and the interest rates that banks must pay to access funding in financial markets – which influence mortgage rates for borrowers – become unpredictable.

Banks do not like such uncertainty and they do not like people defaulting on their loans. Rising interest rates and uncertainty increase their risk, reduce the volume of mortgage sales and place downward pressure on their profits.

How banks think about risk

Once you understand this, predicting bank behaviour in the mortgage market becomes a lot easier. Take the period before the global financial crisis of 2008 as an example. In the early 1990s, controls over mortgage lending were relaxed so that, by the early 2000s, mortgage product innovation was a firm trend.

This led to mortgages being offered for 125% of a property’s value, and banks lending people four times their annual salary (or more) to buy a home and allowing self-employed borrowers to “self-certify” their incomes.

The risks were low at this time for two reasons. First, as mortgage criteria became more liberal, it brought more money into the market. This additional money was chasing the same supply of houses, which increased house prices. In this environment, even if people defaulted, banks could easily sell on repossessed houses and so default risks were less of a concern.

Second, banks began to offload their mortgages into the financial markets at this time, passing on the risk of default to investors. This freed up more money for them to lend out as mortgages.

Read more: How bonds work and why everyone is talking about them right now: a finance expert explains[8]

The Bank of England’s base rate also dropped throughout this period[9] from a high of 7.5% in June 1998 to a low of 3.5% in July 2003. People desired housing, mortgage products were many and varied, and house prices were rising – perfect conditions[10] for a booming housing market. Until, of course, the global financial crisis hit in 2008.

The authorities reacted to the financial crisis by firming up the mortgage rules and going back to basics. This meant increasing the capital – or protection – that banks had to hold against the mortgages they had on their books, and strengthening the rules[11] around mortgage products. In essence: goodbye self-certification and 125% loans, hello lower income multiples and bulked-up bank balance sheets.

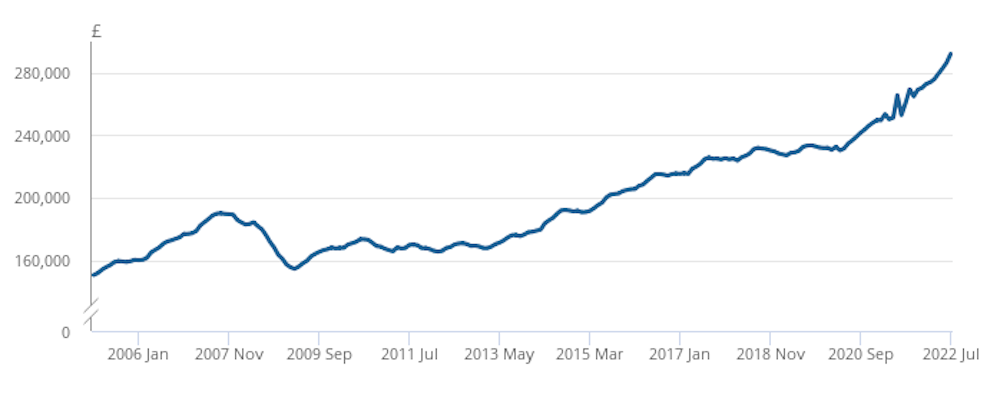

The upshot of these changes was fewer people could qualify to borrow to buy a home, so average UK house prices dropped from more than £188,000 in July 2007 to around £157,000 in January 2009. The damage was so deep that they had only partially recovered some of these losses to reach £167,000 by January 2013.

Average UK house price, Jan 2005-July 2022:

Read more https://theconversation.com/how-to-understand-whats-going-on-with-uk-mortgage-rates-192365